Erin Yurday

Author

Author

19 February 2026

6 min read

Contents

UK Inflation HistoryCurrent Inflation Rates UK Current UK inflation rates block: CPIH +3.2% (12 months to Jan 2026); biggest risers electricity (+5.3%) and restaurants/hotels, with gas (-2.7%) and fuel (-2.2%) cheaper.What's the real impact of inflation on household budgets?FAQsThe guidance on this site is based on our own analysis and is meant to help you identify options and narrow down your choices. We do not advise or tell you which product to buy; undertake your own due diligence before entering into any agreement.

Inflation seems to be everywhere right now, with people having to pay more at the pump, to fill their grocery carts, to pay rent or homeowner expenses, and more - it seems like everything costs more now. In this article we run through the latest figures and try to display the data in a few different ways to give our readers a picture of what's really going on. Learn about inflation rates, see inflation history and see which categories have the biggest price rises.

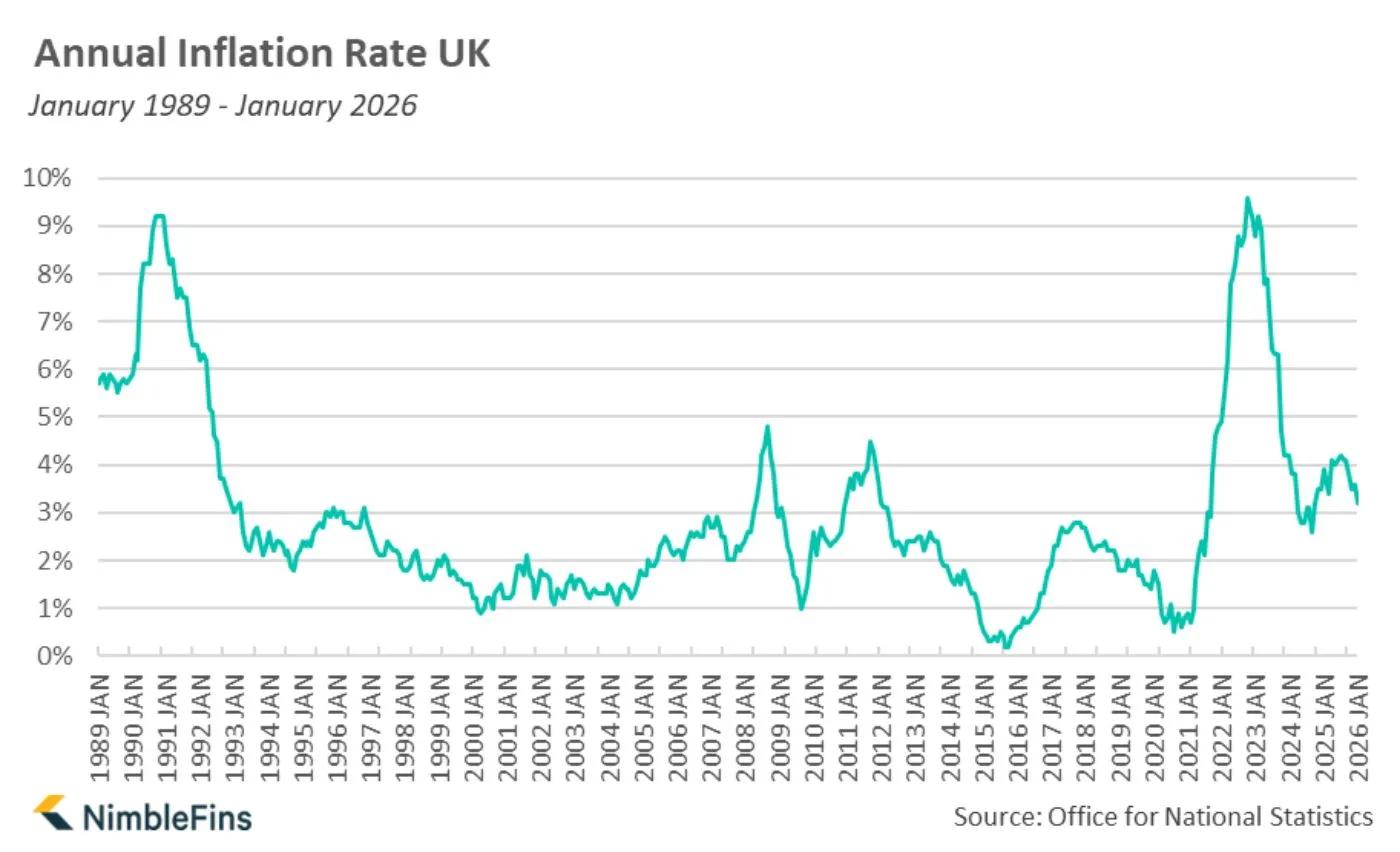

The year 2025 finished with an overall inflation rate of 3.9%. Thankfully, this figure is much lower than we've experienced in recent years (e.g. 7.9% in 2022 and 6.8% in 2023), but 3.9% is still higher compared to historical averages - for example, the average inflation rate from the past 20 years is 2.8%; the average rate going back 30 years is 2.5%.

You can get a feel for where inflation rates are in early 2026 in the following chart (which reflects monthly data from January 1989 through January 2026):

Below are annual rates since 2015, plus the annual rate for April 2022 so you can see how much the inflation rate has jumped up in 2022. Currently, 2026 is starting off with a lower inflation rate of 3.2% (for January).

UK Inflation Rates | Annual Rate |

2015 | 0.4% |

2016 | 1.0% |

2017 | 2.6% |

2018 | 2.3% |

2019 | 1.7% |

2020 | 1.0% |

2021 | 2.5% |

2022 | 7.9% |

2023 | 6.8% |

2024 | 3.3% |

2025 | 3.9% |

2026 (Jan) | 3.2% |

The Inflation Index, which uses 2015 as a reference year, shows the history of how prices have changed over time, and is especially useful for visualising changes across different categories of household spending.

(How does an index work? A base year is chosen where the index is 100. In this case, the base year is 2015. The index values go up or down from 100, according to the mean percentage increases or decreases. A percentage increase nudges the index number above 100, and a percentage decrease drops the index number below 100. You can look forward or backward in time from the reference year.)

The chart below displays inflation history via the index from 2015 (the reference year when all categories were essentially marked at 100) until January 2026. As you can see, the biggest price increases have occurred in the following 5 categories: alcohol/tobacco, education, restaurants/hotels, food, and housing (including water, gas and electricity).

Now let's dig into inflation rates for different areas of the household budget. Which areas have been hit hardest over the past year? Here is a recap of inflation rates from January 2025 - January 2026.

The results are pretty consistent with the index chart above (which shows the inflation data over a longer period, since 2015).

In the past year, ending January 2026, electricity costs have risen the most (+5.3%) followed by restaurants/hotels (+5.3%) and then alcoholic beverages/tobacco and communication (both +4.6%)

On the other hand, gas for the home and petrol for vehicles has gotten cheaper (-2.7% and -2.2%, respectively)!

Inflation Rate | Details | 12-month change to January 2026 |

CPIH (overall index) | 3.2% | |

Transport | 2.7% | |

Fuels and lubricants | -2.2% | |

New cars | 1.8% | |

Second hand cars | 1.1% | |

Motorcycles and bicycles | -0.8% | |

Furniture, household equipment and maintenance | -0.5% | |

Furniture and furnishings | -0.3% | |

Glassware, tableware and household utensils | -2.0% | |

Clothing and footwear | 0.0% | |

Restaurants and hotels | 4.1% | |

Restaurants and hotels | Restaurants & cafes | 4.8% |

Accommodation services | 1.1% | |

Food and non-alcoholic beverages | 3.6% | |

Recreation and culture | 2.6% | |

Alcoholic beverages and tobacco | 4.6% | |

Housing, water, electricity, gas and other fuels | 4.2% | |

Housing, water, electricity, gas and other fuels | Electricity | 5.3% |

Gas | -2.7% | |

Education | 5.1% | |

Health | 3.1% | |

Communication | 4.6% |

We get into more detail for some of these broad budget categories below.

Cost-of-living increases for transport-related spending are primarily due to rises in spare parts/accessories (+5.4%) as well as maintenance costs (+5.2%).

In contrast, motorists are now paying less for fuel compared to one year ago (-2.2%).

Transport Inflation | 12 months to January 2026 |

New cars | 1.8% |

Second hand cars | 1.1% |

Motorcycles and bicycles | -0.9% |

Operation of personal transport equipment | 3.7% |

Spare parts and accessories | 5.4% |

Fuels and lubricants | -2.2% |

Maintenance and repairs | 5.2% |

Transport services | 2.7% |

Passenger transport by railway | 4.5% |

Passenger transport by road | 2.7% |

Passenger transport by air | 0.6% |

Passenger transport by sea and inland waterway | 1.5% |

Rents and housing ownership costs are up 3.1% and 3.9%, respectively - while these may seem like somewhat reasonable numbers relative to other figures mentioned here, given that rent/homeowner costs are such a large proportion of the typical household's expenditures, a small-ish percentage increase of a large absolute number means a big impact for the typical household. Added to that, there is the huge uptick in water prices (+26.1%) as well as significant rises for electricity (+5.3%) and council taxes (+5.4%).

Housing Inflation | 12 months to January 2026 |

Actual rentals for housing | 3.1% |

Owner occupiers housing costs | 3.9% |

Regular maintenance and repair of the dwelling | 0.5% |

Materials for maintenance and repair | 0.2% |

Services for maintenance and repair | 0.6% |

Water supply and misc. services for the dwelling | 26.1% |

Water supply | 26.3% |

Sewerage collection | 26.0% |

Electricity, gas and other fuels | 2.1% |

Electricity | 5.3% |

Gas | -2.7% |

Liquid fuels | -7.0% |

Solid fuels | -0.5% |

Council tax and rates | 5.4% |

After serious price rises a few years ago, some insurance rates actually declined in 2025 - namely, home contents insurance (-15.8%!).

Confusingly, the ONS inflation data shows transport insurance up with a 4% inflation rate, but the ABI reported that motor insurance rates had dropped to £559 for comprehensive policies in Q4 2025, which is 10.2% lower than the same period one year earlier. We're not sure what to make of this conflicting data regarding the cost of motor insurance.

Insurance Inflation | 12 months to January 2026 |

Insurance | 1.9% |

House contents insurance | -15.8% |

Health insurance | 4.2% |

Transport insurance | 4.0% |

Inflation rates are one thing - but what's the real out-of-pocket impact on regular households? How much more money does it actually cost to live now compared to a year ago? Or what might we need to spend to maintain the same quality of life a year from now?

To think about this, we've applied the most recently inflation stat (+3.2% in January 2026) to a range of monthly household budgets. This shows us how much more a household might need to spend in order to buy the same basket of goods and services.

For this exercise, we started by looking at the average household budget, which we calculate to be £2,870 per month. Applying 3.2% inflation to this figure tells us that households with spending around this level may need an extra £92 per month to maintain the same standard of living.

A household spending £2,000 a month would be impacted by £64 per month.

A household spending £5,000 a month would need an extra £160 per month now.

Here's what we found:

Household budget (per month | Additional monthly costs at 3.2% inflation |

£1,500 | £48 |

£2,000 | £64 |

£2,500 | £80 |

£2,870 | £92 |

£3,500 | £112 |

£5,000 | £160 |

£7,000 | £224 |

£10,000 | £320 |

These examples are illustrative and the actual impact will depend on individual spending patterns and which costs each household faces.

As of January 2026, the current inflation rate in the UK was 3.2%, down from an average of 3.9% for 2025.

Inflation is a measure of how much prices have increased. Usually, it shows the change from a year ago, so a 6% inflation rate would mean that prices are now 4% higher than they were a year ago. For example, if a tv cost £100 last year, this year it would cost £104.

In a period of higher inflation, interest rates are usually raised which has the effect of making borrowing more expensive - as a result, people borrow less and have less money to spend. This in turn can help to lower inflation rates. Interest rates are usually changed by central banks like the Bank of England in response to inflation, to keep inflation in check.

Author

19 February 2026

6 min read

Contents

UK Inflation HistoryCurrent Inflation Rates UK Current UK inflation rates block: CPIH +3.2% (12 months to Jan 2026); biggest risers electricity (+5.3%) and restaurants/hotels, with gas (-2.7%) and fuel (-2.2%) cheaper.What's the real impact of inflation on household budgets?FAQsThe guidance on this site is based on our own analysis and is meant to help you identify options and narrow down your choices. We do not advise or tell you which product to buy; undertake your own due diligence before entering into any agreement.

Author

19 February 2026

6 min read

Contents

UK Inflation HistoryCurrent Inflation Rates UK Current UK inflation rates block: CPIH +3.2% (12 months to Jan 2026); biggest risers electricity (+5.3%) and restaurants/hotels, with gas (-2.7%) and fuel (-2.2%) cheaper.What's the real impact of inflation on household budgets?FAQsThe guidance on this site is based on our own analysis and is meant to help you identify options and narrow down your choices. We do not advise or tell you which product to buy; undertake your own due diligence before entering into any agreement.

Inflation seems to be everywhere right now, with people having to pay more at the pump, to fill their grocery carts, to pay rent or homeowner expenses, and more - it seems like everything costs more now. In this article we run through the latest figures and try to display the data in a few different ways to give our readers a picture of what's really going on. Learn about inflation rates, see inflation history and see which categories have the biggest price rises.

The year 2025 finished with an overall inflation rate of 3.9%. Thankfully, this figure is much lower than we've experienced in recent years (e.g. 7.9% in 2022 and 6.8% in 2023), but 3.9% is still higher compared to historical averages - for example, the average inflation rate from the past 20 years is 2.8%; the average rate going back 30 years is 2.5%.

You can get a feel for where inflation rates are in early 2026 in the following chart (which reflects monthly data from January 1989 through January 2026):

Below are annual rates since 2015, plus the annual rate for April 2022 so you can see how much the inflation rate has jumped up in 2022. Currently, 2026 is starting off with a lower inflation rate of 3.2% (for January).

UK Inflation Rates | Annual Rate |

2015 | 0.4% |

2016 | 1.0% |

2017 | 2.6% |

2018 | 2.3% |

2019 | 1.7% |

2020 | 1.0% |

2021 | 2.5% |

2022 | 7.9% |

2023 | 6.8% |

2024 | 3.3% |

2025 | 3.9% |

2026 (Jan) | 3.2% |

The Inflation Index, which uses 2015 as a reference year, shows the history of how prices have changed over time, and is especially useful for visualising changes across different categories of household spending.

(How does an index work? A base year is chosen where the index is 100. In this case, the base year is 2015. The index values go up or down from 100, according to the mean percentage increases or decreases. A percentage increase nudges the index number above 100, and a percentage decrease drops the index number below 100. You can look forward or backward in time from the reference year.)

The chart below displays inflation history via the index from 2015 (the reference year when all categories were essentially marked at 100) until January 2026. As you can see, the biggest price increases have occurred in the following 5 categories: alcohol/tobacco, education, restaurants/hotels, food, and housing (including water, gas and electricity).

Now let's dig into inflation rates for different areas of the household budget. Which areas have been hit hardest over the past year? Here is a recap of inflation rates from January 2025 - January 2026.

The results are pretty consistent with the index chart above (which shows the inflation data over a longer period, since 2015).

In the past year, ending January 2026, electricity costs have risen the most (+5.3%) followed by restaurants/hotels (+5.3%) and then alcoholic beverages/tobacco and communication (both +4.6%)

On the other hand, gas for the home and petrol for vehicles has gotten cheaper (-2.7% and -2.2%, respectively)!

Inflation Rate | Details | 12-month change to January 2026 |

CPIH (overall index) | 3.2% | |

Transport | 2.7% | |

Fuels and lubricants | -2.2% | |

New cars | 1.8% | |

Second hand cars | 1.1% | |

Motorcycles and bicycles | -0.8% | |

Furniture, household equipment and maintenance | -0.5% | |

Furniture and furnishings | -0.3% | |

Glassware, tableware and household utensils | -2.0% | |

Clothing and footwear | 0.0% | |

Restaurants and hotels | 4.1% | |

Restaurants and hotels | Restaurants & cafes | 4.8% |

Accommodation services | 1.1% | |

Food and non-alcoholic beverages | 3.6% | |

Recreation and culture | 2.6% | |

Alcoholic beverages and tobacco | 4.6% | |

Housing, water, electricity, gas and other fuels | 4.2% | |

Housing, water, electricity, gas and other fuels | Electricity | 5.3% |

Gas | -2.7% | |

Education | 5.1% | |

Health | 3.1% | |

Communication | 4.6% |

We get into more detail for some of these broad budget categories below.

Cost-of-living increases for transport-related spending are primarily due to rises in spare parts/accessories (+5.4%) as well as maintenance costs (+5.2%).

In contrast, motorists are now paying less for fuel compared to one year ago (-2.2%).

Transport Inflation | 12 months to January 2026 |

New cars | 1.8% |

Second hand cars | 1.1% |

Motorcycles and bicycles | -0.9% |

Operation of personal transport equipment | 3.7% |

Spare parts and accessories | 5.4% |

Fuels and lubricants | -2.2% |

Maintenance and repairs | 5.2% |

Transport services | 2.7% |

Passenger transport by railway | 4.5% |

Passenger transport by road | 2.7% |

Passenger transport by air | 0.6% |

Passenger transport by sea and inland waterway | 1.5% |

Rents and housing ownership costs are up 3.1% and 3.9%, respectively - while these may seem like somewhat reasonable numbers relative to other figures mentioned here, given that rent/homeowner costs are such a large proportion of the typical household's expenditures, a small-ish percentage increase of a large absolute number means a big impact for the typical household. Added to that, there is the huge uptick in water prices (+26.1%) as well as significant rises for electricity (+5.3%) and council taxes (+5.4%).

Housing Inflation | 12 months to January 2026 |

Actual rentals for housing | 3.1% |

Owner occupiers housing costs | 3.9% |

Regular maintenance and repair of the dwelling | 0.5% |

Materials for maintenance and repair | 0.2% |

Services for maintenance and repair | 0.6% |

Water supply and misc. services for the dwelling | 26.1% |

Water supply | 26.3% |

Sewerage collection | 26.0% |

Electricity, gas and other fuels | 2.1% |

Electricity | 5.3% |

Gas | -2.7% |

Liquid fuels | -7.0% |

Solid fuels | -0.5% |

Council tax and rates | 5.4% |

After serious price rises a few years ago, some insurance rates actually declined in 2025 - namely, home contents insurance (-15.8%!).

Confusingly, the ONS inflation data shows transport insurance up with a 4% inflation rate, but the ABI reported that motor insurance rates had dropped to £559 for comprehensive policies in Q4 2025, which is 10.2% lower than the same period one year earlier. We're not sure what to make of this conflicting data regarding the cost of motor insurance.

Insurance Inflation | 12 months to January 2026 |

Insurance | 1.9% |

House contents insurance | -15.8% |

Health insurance | 4.2% |

Transport insurance | 4.0% |

Inflation rates are one thing - but what's the real out-of-pocket impact on regular households? How much more money does it actually cost to live now compared to a year ago? Or what might we need to spend to maintain the same quality of life a year from now?

To think about this, we've applied the most recently inflation stat (+3.2% in January 2026) to a range of monthly household budgets. This shows us how much more a household might need to spend in order to buy the same basket of goods and services.

For this exercise, we started by looking at the average household budget, which we calculate to be £2,870 per month. Applying 3.2% inflation to this figure tells us that households with spending around this level may need an extra £92 per month to maintain the same standard of living.

A household spending £2,000 a month would be impacted by £64 per month.

A household spending £5,000 a month would need an extra £160 per month now.

Here's what we found:

Household budget (per month | Additional monthly costs at 3.2% inflation |

£1,500 | £48 |

£2,000 | £64 |

£2,500 | £80 |

£2,870 | £92 |

£3,500 | £112 |

£5,000 | £160 |

£7,000 | £224 |

£10,000 | £320 |

These examples are illustrative and the actual impact will depend on individual spending patterns and which costs each household faces.

As of January 2026, the current inflation rate in the UK was 3.2%, down from an average of 3.9% for 2025.

Inflation is a measure of how much prices have increased. Usually, it shows the change from a year ago, so a 6% inflation rate would mean that prices are now 4% higher than they were a year ago. For example, if a tv cost £100 last year, this year it would cost £104.

In a period of higher inflation, interest rates are usually raised which has the effect of making borrowing more expensive - as a result, people borrow less and have less money to spend. This in turn can help to lower inflation rates. Interest rates are usually changed by central banks like the Bank of England in response to inflation, to keep inflation in check.

Author

19 February 2026

6 min read

Contents

UK Inflation HistoryCurrent Inflation Rates UK Current UK inflation rates block: CPIH +3.2% (12 months to Jan 2026); biggest risers electricity (+5.3%) and restaurants/hotels, with gas (-2.7%) and fuel (-2.2%) cheaper.What's the real impact of inflation on household budgets?FAQsThe guidance on this site is based on our own analysis and is meant to help you identify options and narrow down your choices. We do not advise or tell you which product to buy; undertake your own due diligence before entering into any agreement.