Erin Yurday

Author

Author

24 January 2026

9 min read

Contents

What is the Minimum Monthly Payment Calculated?How do Credit Cards Calculate Minimum Payment?What is the Floor of the Minimum Monthly Payment?When Does the Floor Kick In?Should You Only Pay the Minimum Each Month?How to Find the Minimum Payment FloorEscaping the Debt SpiralFAQsThe guidance on this site is based on our own analysis and is meant to help you identify options and narrow down your choices. We do not advise or tell you which product to buy; undertake your own due diligence before entering into any agreement.

CREDIT CARDS BY FEATURES

Best Credit Cards for Bad CreditBest Balance Transfer Credit CardsBest 0% Interest Credit Cards for PurchasesBest Travel Credit CardsBest Credit Cards with No Annual FeeBest Travel Credit CardsBest Credit Cards for StudentsBest Cashback Credit CardsBest Rewards Credit CardsBest Hotel Rewards Credit CardsHave you ever looked at how the minimum monthly payment on your credit card is calculated? Most people haven’t. In the January 2026 economy, understanding your minimum payment 'floor' is a critical survival skill. With the average UK credit card interest rate (APR) hitting 24.66% - the highest in over 30 years - and the average household credit card balance reaching £2,601, the 'minimum payment trap' is no longer just a slow way to pay; it is a multi-thousand-pound risk that can keep families in debt for decades.

We may receive commission if you click through or take out a product.

Your minimum payment is largely dictated by your interest rate, as well as your outstanding balance and any default charges.

While the national credit card rate average sits at 24.66%, those with poor credit now typically face an APR of 36.2%. For certain credit-builder products, rates can even climb to a staggering 59.9% variable. These record-high benchmarks mean that the 'interest' portion of your minimum payment is now significantly larger, leaving less of your money to actually reduce your debt.

Each credit card company has their own rules for calculating your minimum monthly payment, but typically a minimum monthly payment is calculated as the highest of:

£5 (or the full outstanding balance if it's less than £5) - this is called the "floor"

2.5% of the balance

1% of the balance plus interest and default charges

The minimum monthly payment "floor" is a small amount that your minimum monthly payment will never fall below. Most credit cards impose a floor of only £5 but some credit card providers (e.g., Tesco Bank, Amex and Vanquis) have a higher floor between £10 and £25.

At first glance, a smaller floor may seem better - but it’s not. The smaller the floor, the longer it will take to pay back credit card debt and the more interest you will pay along the way. A higher floor helps you pay back debt sooner and pay less in interest charges.

Because interest compounds so much faster at these rates, a higher floor prevents thousands more in interest from accruing compared to a lower floor. With 10% of UK adults currently having no cash savings, these interest savings aren't just a 'bonus' - they are a vital pillar of financial resilience in an expensive market.

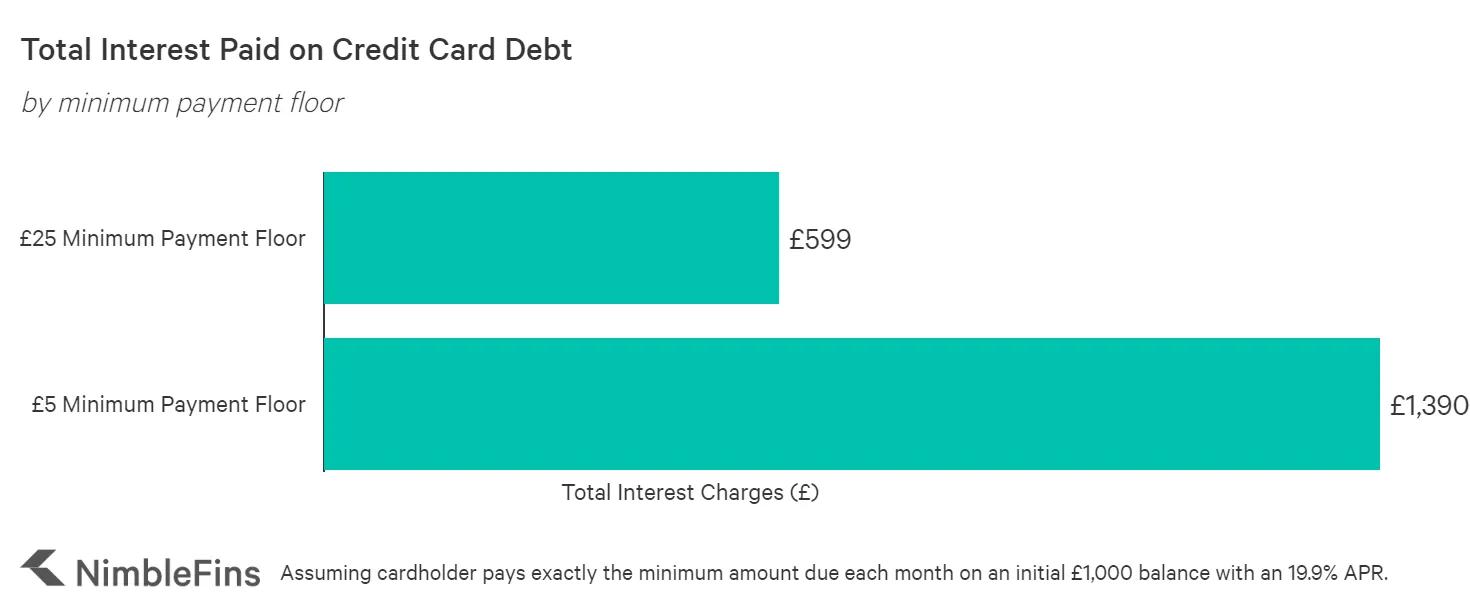

The following chart compares the total interest paid over time for a £5 floor and a £25 floor, on a £1,000 initial balance where only the minimum payment is made each month. In this case, the higher floor saves the card holder a whopping £770 in interest charges over the life of the debt - that's nearly as much as the original balance! And at a higher APR, the results would be even more staggering.

If you don't add to credit card balances, your minimum payment should decline over time as you reduce the amount owed. Why? The minimum payment is (in part) calculated as a percentage of the balance. So as the balance drops so do the minimum payments - until the "floor" is reached.

For most credit cards charging 19.9% APR, a £25 floor would kick in for balances below £1,000 or so (if your minimum payment is calculated using 1% of the amount owed, not a higher amount). This means that each month the minimum payment would be a fixed £25 - it would not drop below £25 as you work to pay down the balance from £1,000 to zero.

A card with a lower floor of £5 would take much longer to pay off, because the minimum payment would continue to decline until the balance falls to around £200, at which point the £5 floor kicks in.

Floor | Floor Kicks in for Balances Below… | Time to Pay Debt | Total Interest Charges |

£5 | £200 | 18 years 6 months | £1,390 |

£25 | £1,000 | 5 years 4 months | £599 |

The following chart shows how the time to become debt free is drastically reduced if the minimum payment floor is higher, for those who only pay the minimum amount due each month.

With the 2026 national average now at 24.66% APR, the 'floor' triggers much sooner. At this rate, a £25 floor will generally kick in for balances below approximately £820. This is because at a higher APR, the interest and percentage-based portion of your payment stays above £25 for longer.

While it's critical to pay the minimum amount each month (to avoid default charges, being reported to credit agencies, etc.), it's actually really important to pay MORE than the minimum each and every month. The more you pay, the better. Paying as much as you can over the minimum each month will:

Reduce the total amount of interest you pay over the life of the debt

Reduce the time to become debt free.

Generally speaking, credit cards are an expensive form of debt and balances should be reduced as soon as possible, which you can help along by paying more than the minimum each month.

The minimum payment floor can be found in the Summary Box for a credit card, in the section labelled, "Minimum Payment." If you're someone who might pay only the minimum amount each month, you may want to consider a card with a £25 minimum payment floor to save money in interest charges in the long run. If you want to find a minimum payment for a card, you can oftentimes find it by Googling the brand and product line of the card, plus "summary box". Most credit card companies provide easy access to the summary box (as they should, in our opinion).

The following table shows the minimum monthly payment floor for a list of UK credit cards. This alphabetical list is not exhaustive, is subject to change and may vary from card to card; this list is only meant to illustrate the range of floors available in the UK market.

Card Card Provider | Minimum Monthly Payment Floor |

American Express | £25 |

Aqua | £5 |

Asda | £5 |

Barclays | £5 |

Halifax | £5 |

HSBC | £5 |

Lloyds | £5 |

Marbles | £5 |

MBNA | £25 |

Partnership Card | £5 |

RBS | £5 |

Tesco | £25 |

Vanquis | £10 |

Virgin Money | £25 |

For many cards the payment may be a formula, e.g. for the AMEX Platinum Cashback, it's the sum of all interest, default fees, and 1/12th of the annual fee, plus 2% of the remaining balance

For more information on the implications of minimum payment floors, please see our Top Tips to Reduce Credit Card Interest Payments.

As of 2026, 24% of UK adults are defined as having 'low financial resilience', a precarious position given that average non-mortgage debt has climbed to £18,392. In this climate, simply paying the minimum is a recipe for a debt spiral. Actively aiming to pay even £10 or £20 above your 'floor' each month is one of the most effective ways for modern households to reclaim their financial freedom.

Disclaimer: ClearScore is a credit broker, not a lender, and does not cover the whole of the market. The offers shown are drawn from ClearScore's panel of lenders and partners, so other products may be available elsewhere that are not featured here. ClearScore may receive a commission from the lender if you take out a product through the service. This does not affect the price you pay.

If you pay less than the minimum payment on your credit card, you will be charged a default fee (typically £12) and your late payment may be reported to the credit agencies, hurting your credit score. Also, your interest rate could rise if the card company thinks you're a higher risk due to your insufficient payment.

If you can't make the minimum payment on your credit card, the first step is to call your card company to ask if they can pause your payments. They will be more likely to pause payments if your situation is temporary (e.g., you just lost your job or you're making priority payments on rent arrears). Also, look into resources available to help those with problem debt.

Yes, all credit cards have a minimum payment.

Yes, 0 credit cards still have a minimum payment. During the 0% interest phase the minimum payment will not include any interest charges and your minimum payment will go towards reducing the amount you owe.

The minimum payment due is an amount you pay to your credit card each month that typically includes a partial repayment of the amount you owe, interest charges and any default fees.

The minimum payment on Amex credit cards like the BA Amex Premium Plus is the higher of the following amounts: 1) £25 (or the total amount you owe if less) or 2) any interest, default fees, repayment protection insurance and 1/12th of any annual cardmembership fee or the full monthly fee plus 2% of the amount you owe.

The minimum payment on Halifax credit cards is the higher of the following amounts: 1) £5 (or the full amount you owe if less) or 2) any interest and default charges payable plus 1% of the total balance you owe.

The minimum payment on Tesco credit cards is the higher of the following amounts: 1) £25 plus arrears from previous statement (or the full amount you owe if less) or 2) any interest and default charges payable plus 1% of the total balance you owe plus arrears or 3) the amount you owe over your credit limit including over limit fees.

The minimum payment on Vanquis credit cards like the Chrome is the higher of the following amounts: 1) £10 (or the full amount you owe if less) or 2) any interest and default charges payable plus 2.5% or 3% of the total balance you owe (depending on your APR).

The minimum payment on Santander credit cards like the Zero is the higher of the following amounts: 1) £5 (or the full amount you owe if less) or 2) any interest and default charges payable plus 1% of the total balance you owe, plus any arrears.

The minimum payment on Capital One credit cards is the higher of the following amounts: 1) £5 (or the full amount you owe if less) or 2) any interest and default charges payable, 1/12 of any annual fee, plus 3% of the total balance you owe.

Author

24 January 2026

9 min read

Contents

What is the Minimum Monthly Payment Calculated?How do Credit Cards Calculate Minimum Payment?What is the Floor of the Minimum Monthly Payment?When Does the Floor Kick In?Should You Only Pay the Minimum Each Month?How to Find the Minimum Payment FloorEscaping the Debt SpiralFAQsThe guidance on this site is based on our own analysis and is meant to help you identify options and narrow down your choices. We do not advise or tell you which product to buy; undertake your own due diligence before entering into any agreement.

CREDIT CARDS BY FEATURES

Best Credit Cards for Bad CreditBest Balance Transfer Credit CardsBest 0% Interest Credit Cards for PurchasesBest Travel Credit CardsBest Credit Cards with No Annual FeeBest Travel Credit CardsBest Credit Cards for StudentsBest Cashback Credit CardsBest Rewards Credit CardsBest Hotel Rewards Credit CardsAuthor

24 January 2026

9 min read

Contents

What is the Minimum Monthly Payment Calculated?How do Credit Cards Calculate Minimum Payment?What is the Floor of the Minimum Monthly Payment?When Does the Floor Kick In?Should You Only Pay the Minimum Each Month?How to Find the Minimum Payment FloorEscaping the Debt SpiralFAQsThe guidance on this site is based on our own analysis and is meant to help you identify options and narrow down your choices. We do not advise or tell you which product to buy; undertake your own due diligence before entering into any agreement.

CREDIT CARDS BY FEATURES

Best Credit Cards for Bad CreditBest Balance Transfer Credit CardsBest 0% Interest Credit Cards for PurchasesBest Travel Credit CardsBest Credit Cards with No Annual FeeBest Travel Credit CardsBest Credit Cards for StudentsBest Cashback Credit CardsBest Rewards Credit CardsBest Hotel Rewards Credit CardsHave you ever looked at how the minimum monthly payment on your credit card is calculated? Most people haven’t. In the January 2026 economy, understanding your minimum payment 'floor' is a critical survival skill. With the average UK credit card interest rate (APR) hitting 24.66% - the highest in over 30 years - and the average household credit card balance reaching £2,601, the 'minimum payment trap' is no longer just a slow way to pay; it is a multi-thousand-pound risk that can keep families in debt for decades.

We may receive commission if you click through or take out a product.

Your minimum payment is largely dictated by your interest rate, as well as your outstanding balance and any default charges.

While the national credit card rate average sits at 24.66%, those with poor credit now typically face an APR of 36.2%. For certain credit-builder products, rates can even climb to a staggering 59.9% variable. These record-high benchmarks mean that the 'interest' portion of your minimum payment is now significantly larger, leaving less of your money to actually reduce your debt.

Each credit card company has their own rules for calculating your minimum monthly payment, but typically a minimum monthly payment is calculated as the highest of:

£5 (or the full outstanding balance if it's less than £5) - this is called the "floor"

2.5% of the balance

1% of the balance plus interest and default charges

The minimum monthly payment "floor" is a small amount that your minimum monthly payment will never fall below. Most credit cards impose a floor of only £5 but some credit card providers (e.g., Tesco Bank, Amex and Vanquis) have a higher floor between £10 and £25.

At first glance, a smaller floor may seem better - but it’s not. The smaller the floor, the longer it will take to pay back credit card debt and the more interest you will pay along the way. A higher floor helps you pay back debt sooner and pay less in interest charges.

Because interest compounds so much faster at these rates, a higher floor prevents thousands more in interest from accruing compared to a lower floor. With 10% of UK adults currently having no cash savings, these interest savings aren't just a 'bonus' - they are a vital pillar of financial resilience in an expensive market.

The following chart compares the total interest paid over time for a £5 floor and a £25 floor, on a £1,000 initial balance where only the minimum payment is made each month. In this case, the higher floor saves the card holder a whopping £770 in interest charges over the life of the debt - that's nearly as much as the original balance! And at a higher APR, the results would be even more staggering.

If you don't add to credit card balances, your minimum payment should decline over time as you reduce the amount owed. Why? The minimum payment is (in part) calculated as a percentage of the balance. So as the balance drops so do the minimum payments - until the "floor" is reached.

For most credit cards charging 19.9% APR, a £25 floor would kick in for balances below £1,000 or so (if your minimum payment is calculated using 1% of the amount owed, not a higher amount). This means that each month the minimum payment would be a fixed £25 - it would not drop below £25 as you work to pay down the balance from £1,000 to zero.

A card with a lower floor of £5 would take much longer to pay off, because the minimum payment would continue to decline until the balance falls to around £200, at which point the £5 floor kicks in.

Floor | Floor Kicks in for Balances Below… | Time to Pay Debt | Total Interest Charges |

£5 | £200 | 18 years 6 months | £1,390 |

£25 | £1,000 | 5 years 4 months | £599 |

The following chart shows how the time to become debt free is drastically reduced if the minimum payment floor is higher, for those who only pay the minimum amount due each month.

With the 2026 national average now at 24.66% APR, the 'floor' triggers much sooner. At this rate, a £25 floor will generally kick in for balances below approximately £820. This is because at a higher APR, the interest and percentage-based portion of your payment stays above £25 for longer.

While it's critical to pay the minimum amount each month (to avoid default charges, being reported to credit agencies, etc.), it's actually really important to pay MORE than the minimum each and every month. The more you pay, the better. Paying as much as you can over the minimum each month will:

Reduce the total amount of interest you pay over the life of the debt

Reduce the time to become debt free.

Generally speaking, credit cards are an expensive form of debt and balances should be reduced as soon as possible, which you can help along by paying more than the minimum each month.

The minimum payment floor can be found in the Summary Box for a credit card, in the section labelled, "Minimum Payment." If you're someone who might pay only the minimum amount each month, you may want to consider a card with a £25 minimum payment floor to save money in interest charges in the long run. If you want to find a minimum payment for a card, you can oftentimes find it by Googling the brand and product line of the card, plus "summary box". Most credit card companies provide easy access to the summary box (as they should, in our opinion).

The following table shows the minimum monthly payment floor for a list of UK credit cards. This alphabetical list is not exhaustive, is subject to change and may vary from card to card; this list is only meant to illustrate the range of floors available in the UK market.

Card Card Provider | Minimum Monthly Payment Floor |

American Express | £25 |

Aqua | £5 |

Asda | £5 |

Barclays | £5 |

Halifax | £5 |

HSBC | £5 |

Lloyds | £5 |

Marbles | £5 |

MBNA | £25 |

Partnership Card | £5 |

RBS | £5 |

Tesco | £25 |

Vanquis | £10 |

Virgin Money | £25 |

For many cards the payment may be a formula, e.g. for the AMEX Platinum Cashback, it's the sum of all interest, default fees, and 1/12th of the annual fee, plus 2% of the remaining balance

For more information on the implications of minimum payment floors, please see our Top Tips to Reduce Credit Card Interest Payments.

As of 2026, 24% of UK adults are defined as having 'low financial resilience', a precarious position given that average non-mortgage debt has climbed to £18,392. In this climate, simply paying the minimum is a recipe for a debt spiral. Actively aiming to pay even £10 or £20 above your 'floor' each month is one of the most effective ways for modern households to reclaim their financial freedom.

Disclaimer: ClearScore is a credit broker, not a lender, and does not cover the whole of the market. The offers shown are drawn from ClearScore's panel of lenders and partners, so other products may be available elsewhere that are not featured here. ClearScore may receive a commission from the lender if you take out a product through the service. This does not affect the price you pay.

If you pay less than the minimum payment on your credit card, you will be charged a default fee (typically £12) and your late payment may be reported to the credit agencies, hurting your credit score. Also, your interest rate could rise if the card company thinks you're a higher risk due to your insufficient payment.

If you can't make the minimum payment on your credit card, the first step is to call your card company to ask if they can pause your payments. They will be more likely to pause payments if your situation is temporary (e.g., you just lost your job or you're making priority payments on rent arrears). Also, look into resources available to help those with problem debt.

Yes, all credit cards have a minimum payment.

Yes, 0 credit cards still have a minimum payment. During the 0% interest phase the minimum payment will not include any interest charges and your minimum payment will go towards reducing the amount you owe.

The minimum payment due is an amount you pay to your credit card each month that typically includes a partial repayment of the amount you owe, interest charges and any default fees.

The minimum payment on Amex credit cards like the BA Amex Premium Plus is the higher of the following amounts: 1) £25 (or the total amount you owe if less) or 2) any interest, default fees, repayment protection insurance and 1/12th of any annual cardmembership fee or the full monthly fee plus 2% of the amount you owe.

The minimum payment on Halifax credit cards is the higher of the following amounts: 1) £5 (or the full amount you owe if less) or 2) any interest and default charges payable plus 1% of the total balance you owe.

The minimum payment on Tesco credit cards is the higher of the following amounts: 1) £25 plus arrears from previous statement (or the full amount you owe if less) or 2) any interest and default charges payable plus 1% of the total balance you owe plus arrears or 3) the amount you owe over your credit limit including over limit fees.

The minimum payment on Vanquis credit cards like the Chrome is the higher of the following amounts: 1) £10 (or the full amount you owe if less) or 2) any interest and default charges payable plus 2.5% or 3% of the total balance you owe (depending on your APR).

The minimum payment on Santander credit cards like the Zero is the higher of the following amounts: 1) £5 (or the full amount you owe if less) or 2) any interest and default charges payable plus 1% of the total balance you owe, plus any arrears.

The minimum payment on Capital One credit cards is the higher of the following amounts: 1) £5 (or the full amount you owe if less) or 2) any interest and default charges payable, 1/12 of any annual fee, plus 3% of the total balance you owe.

Author

24 January 2026

9 min read

Contents

What is the Minimum Monthly Payment Calculated?How do Credit Cards Calculate Minimum Payment?What is the Floor of the Minimum Monthly Payment?When Does the Floor Kick In?Should You Only Pay the Minimum Each Month?How to Find the Minimum Payment FloorEscaping the Debt SpiralFAQsThe guidance on this site is based on our own analysis and is meant to help you identify options and narrow down your choices. We do not advise or tell you which product to buy; undertake your own due diligence before entering into any agreement.

CREDIT CARDS BY FEATURES

Best Credit Cards for Bad CreditBest Balance Transfer Credit CardsBest 0% Interest Credit Cards for PurchasesBest Travel Credit CardsBest Credit Cards with No Annual FeeBest Travel Credit CardsBest Credit Cards for StudentsBest Cashback Credit CardsBest Rewards Credit CardsBest Hotel Rewards Credit Cards